Market Update- 18th December 2024

Dec 18, 2024

Frankie’s Winter Market Update 2024

Welcome to Frankie’s bi-weekly market update, crafted for our members to share key global market insights, and financial news. Managing wealth takes smart planning and informed decisions, and we’re here to help with expert analysis, trends, and tips to guide your financial journey. In this edition, we are reflecting over the past twelve months as 2024 draws to a close, looking at the winners and the losers of the year, as well as summarizing the reactions to the recent Autumn Budget.

Market Overview:

Our first event of 2024, was titled ‘Building your Money Mindset’, looking at the opportunities and the challenges of the year ahead. A hot topic was the fact that nearly half the world population was going to the election polls and geo-political uncertainty was leading to many musing of the potential for a volatile year in markets. This was coupled with concerns around inflation and interest rates, with many investment managers predicting that there would be between 3-4 interest rate cuts in 2024.

In reality, 2024 has seen a number of events that I don’t think many truly believed could happen- Donald Trump being re-elected into the Oval Office being one! We have seen Labour government storming to victory this summer in the UK, right-wing politics continuing to gather strength across Europe, inflation moving up and down like a yo-yo and interest rates starting to be cut.

Despite all of this and the challenging geo-political and humanitarian crisis across the globe; markets have on the whole been incredibly buoyant year to date. With the S&P 500 recording some record high days, much of the US market has been driven by the performance of the ‘Magnificent Seven’ who have dominated the market throughout the year. Although as we have approached the end of the year, caution has started to be applied to the ‘Mag 7’ as the voices of concern around concentration, over hyped valuations and decreasing earnings start to grow.

The year 2024 has been a defining period for global financial markets, with inflationary pressures easing, central banks recalibrating monetary policy, and geopolitical events shaping market dynamics.

Key Themes and Market Highlights

Inflation and Interest Rates: Inflation showed signs of moderation globally, stabilising at manageable levels, including in the UK. The Bank of England adopted a measured approach to rate cuts, prioritising economic stability amid ongoing challenges. While the broader move toward rate easing supported financial markets, central banks face a fine balance between fostering growth and addressing persistent inflation risks.

- Currency Markets: The British pound demonstrated remarkable resilience throughout 2024. Despite speculation around potential rate cuts, confidence in UK economic fundamentals has kept sterling strong against major currencies. In contrast, the euro struggled due to aggressive monetary easing by the ECB and ongoing trade uncertainties, particularly regarding potential US tariffs. The US dollar experienced a volatile year, initially depreciating but recovering on post-election optimism.

- Commodities: Precious metals, led by gold and silver, delivered standout performances. Geopolitical tensions, strong central bank demand, and election-related uncertainties drove gold prices up by over 30%, with silver gains exceeding 35%. Natural gas prices also surged amid colder weather forecasts, fueling demand in Europe and Asia. However, oil faced a challenging year due to weak Chinese demand and a global shift toward renewable energy.

- Equities: Global stock markets saw mixed performances, with US markets—particularly the tech sector—leading gains. Innovations in artificial intelligence drove strong earnings, pushing the Nasdaq and S&P 500 to new highs. In the UK, equities remained steady, benefiting from declining inflation and stable corporate earnings. However, concerns around valuations and potential trade tariffs loom large heading into 2025.

Opportunities and Risks for 2025

As we look ahead, several factors are set to shape the market landscape:

- Central Bank Policy: The Bank of England and other central banks are likely to continue measured rate cuts, but any resurgence in inflation could prompt a policy shift. Interest rate differentials will play a key role in currency movements.

- Trade Dynamics: Potential US tariffs and ongoing trade tensions present risks for global markets, particularly for the Eurozone and export-driven sectors.

- Technological Innovation: Advances in AI and emerging technologies offer growth potential, particularly in the tech and innovation-driven sectors.

- Geopolitical Risks: Political uncertainties, from trade disputes to broader geopolitical conflicts, remain unpredictable but could have significant market implications.

The resilience demonstrated by financial markets in 2024 highlights the opportunities that can emerge even in a challenging environment. For UK investors, staying informed on global economic trends, central bank policies, and technological advancements will be crucial in navigating 2025. While risks persist, the coming year presents an opportunity to capitalise on shifting dynamics and identify areas of growth.

UK Autumn Budget Summary

On 30th October, Rachel Reeves, the UK Chancellor, presented the Autumn Budget 2024, providing much-anticipated clarity on the future of the UK’s tax landscape. This Budget, one of the most significant in recent years, featured a range of tax policy announcements. While many measures aligned with previous proposals or expectations, a few unexpected developments were also introduced.

Notably, the majority of the announced changes are yet to take effect, remain subject to amendment, and could be altered pending enactment.

The Office for Budget Responsibility (OBR) published several key forecasts for the next five years, including:

- Public finances are forecast to move into surplus by 2028, aligning with the timeline of the next general election.

- Economic growth is expected to remain below 2% over this period.

- Inflation is projected to stay below 3% for the next five years.

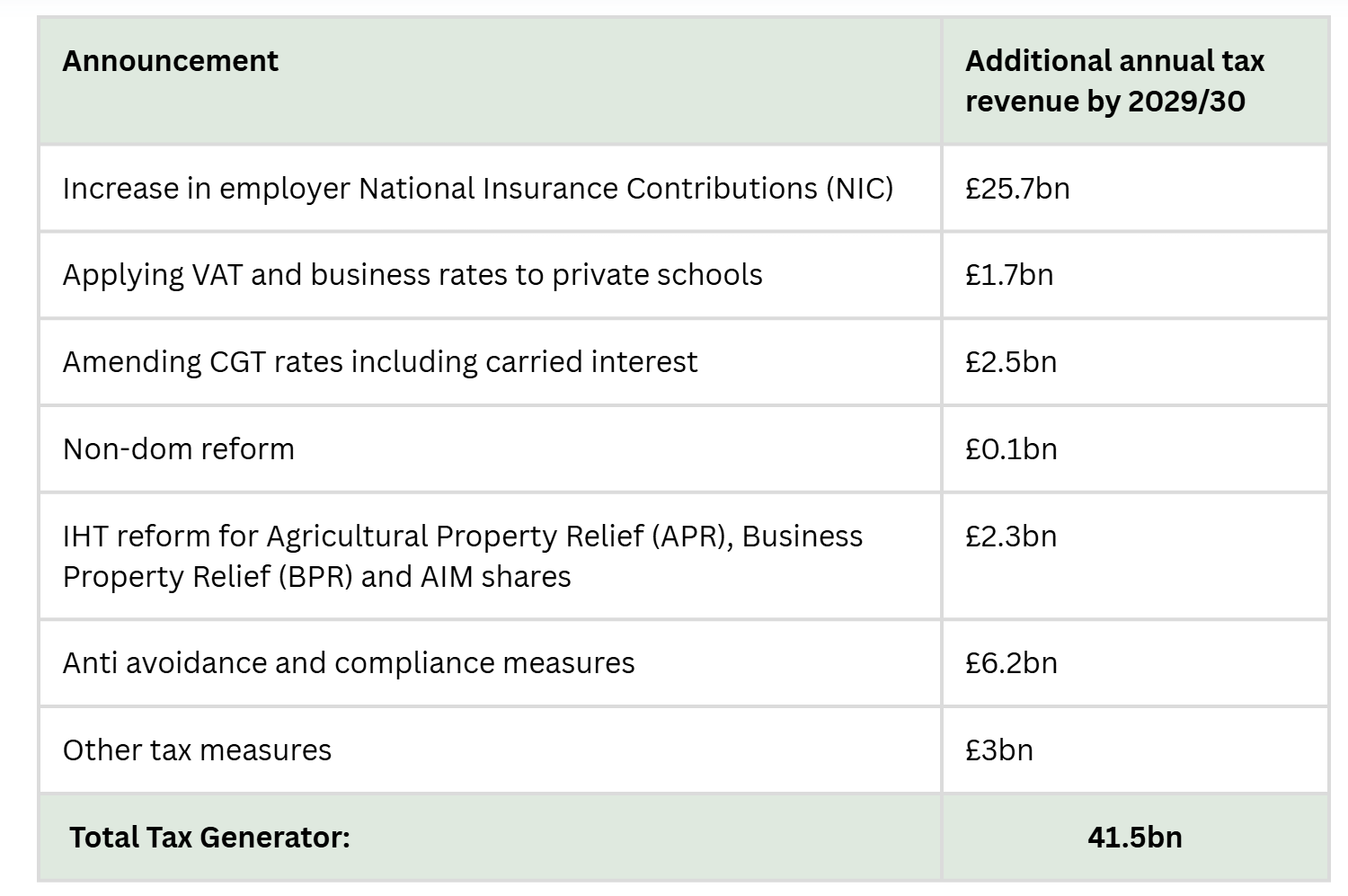

Rachel Reeves stated that the measures outlined in the Budget are expected to generate an additional £40 billion in tax revenues by 2029/30. Further details on this are provided in the table below.

How was the £40bn in tax rise calculated ? Rachel Reeves indicated in her Autumn Budget statement that her announcements would give rise to an additional £40bn in taxes by the end of the current parliament. We have broken out this figure below:

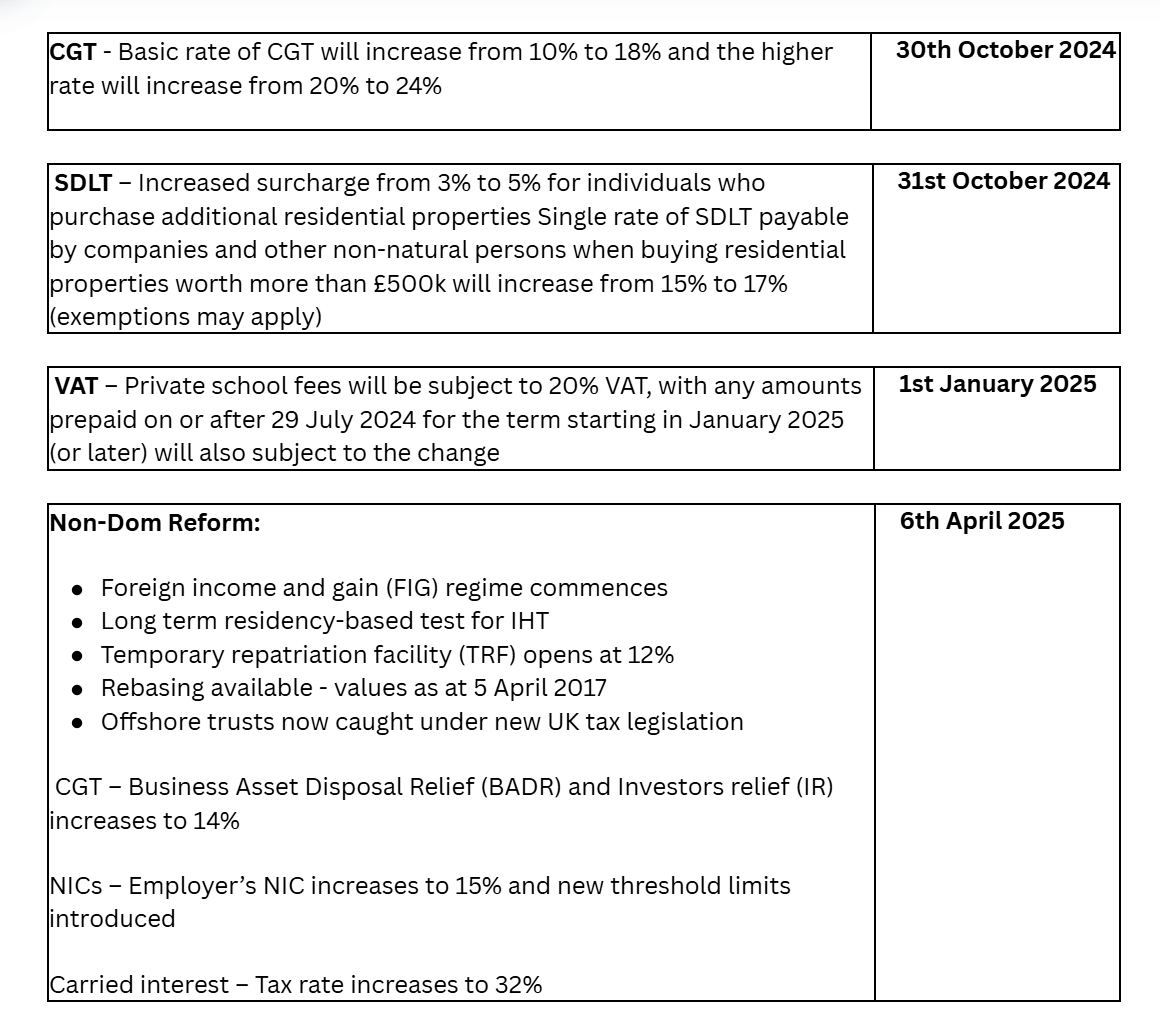

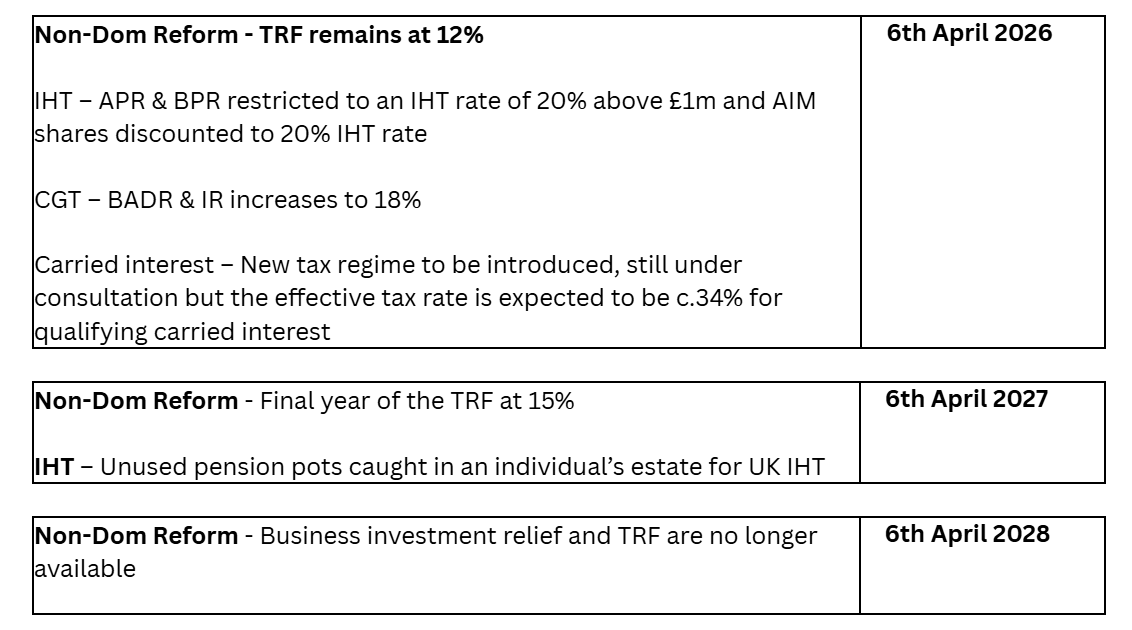

Confirmed timeline for key changes

The Winners and The Losers

Winners

With the highest tax burden in over 30 years, the 2024 Autumn Budget, forecast to raise an additional £40 billion, offers limited opportunities to identify “winners.” However, while the measures have been described as “painful,” their impact will vary across different groups. Below are some of the individuals and sectors that stand to benefit from the announcements:

- UK Domiciled Individuals Living Abroad: The Budget introduces a significant change to the inheritance tax (IHT) rules for UK domiciled individuals who have relocated abroad. Previously, it was challenging to lose UK domicile status for IHT purposes. Under the new residency-based test, UK domiciled expats who have been non-resident for more than 10 out of the last 20 years will no longer fall within the UK IHT scope, except for UK situs assets. Furthermore, eligible individuals returning to the UK may benefit from a 10-year exemption from UK IHT on foreign assets.

- Temporary Residents in the UK: Individuals moving temporarily to the UK can now enjoy their first four years of residency without a UK tax charge on foreign income and gains, provided they were not UK residents in any of the previous 10 tax years. Additionally, these individuals may bring such foreign funds into the UK tax-free, offering a welcome improvement to the current remittance basis rules.

- Support for EIS and VCT Schemes: Investors in the Enterprise Investment Scheme (EIS) and Venture Capital Trusts (VCT) will welcome the 10-year extension of these regimes, which are now set to continue through to April 2035.

- Historic Non-Domiciled Individuals with Offshore Funds: From 6 April 2025, a new Tainted Remittance Facility (TRF) will enable individuals with “tainted” offshore mixed funds to designate these funds and pay UK tax at a reduced rate of 12% for the 2025/26 and 2026/27 tax years, and 15% thereafter. Once taxed, these funds can be remitted to the UK without further tax liabilities or reporting obligations.

- Draught Duty Reduction: While modest, a 1.7% cut to draught beer duty equates to a 1p saving on a pint at the pub, offering a small win for those enjoying the occasional drink.

- Income and NIC Threshold Adjustments: From 2028/29, income tax and National Insurance thresholds will increase in line with inflation, and the State Pension triple lock will remain in place.

- No Wealth Tax or Lifetime Gifting Changes: Despite pre-Budget speculation, there were no announcements introducing a wealth tax, an exit tax for individuals, or changes to lifetime gifting rules. However, this does not preclude the possibility of future amendments. An exit-type tax has been introduced for specific offshore trusts where the settlor leaves the UK.

Losers

On the other side of the £40 billion equation, the Chancellor announced several substantial changes that will significantly impact various groups. Some of the most affected include:

- Pensions: From April 2027, unused pensions will be included in an individual’s IHT estate on death. This creates a difficult decision for those with substantial pension pots who had anticipated passing them on free of IHT: either face income tax on pension withdrawals or risk IHT on the remaining balance upon death. Beneficiaries may also encounter income tax exposure on inherited pensions.

- Capital Gains Tax (CGT): Investors and business owners face an increase in the CGT rate to 24%. While the Chancellor reaffirmed the £1 million Business Asset Disposal Relief (BADR) lifetime limit, the relief will be less valuable as CGT rates rise further—to 14% from April 2025 and 18% from April 2026.

- Business Owners and Farmers: Historically, business and agricultural assets qualified for 100% IHT relief, but this relief will now be capped at an aggregate value of £1 million. Assets exceeding this threshold will receive 50% relief, leaving the remainder subject to IHT at 20% upon death. Notably, this cap and relief can also apply to assets held within trusts, exposing many estates to significant IHT liabilities.

- Employers: The increase in the employer’s National Insurance rate from 13.8% to 15% represents a significant additional cost to businesses. This could lead to reduced employee pay, hiring freezes, or even headcount reductions as businesses absorb the increased burden.

- Stamp Duty Land Tax (SDLT): Purchasers of second homes or buy-to-let properties now face an increase in the SDLT surcharge rate from 3% to 5%, effective from 31 October 2024. The immediate implementation left no time for prospective buyers to complete transactions under the previous rate.

- Inheritance Tax (IHT) for Non-Domiciled Individuals: Current non-doms with large excluded property trusts may now be subject to UK IHT on non-UK assets, reversing protections that were previously available. This is a particularly complex area, which we explore further in the following pages.

Key Financial Dates for 2025 in the UK

Keeping track of key financial dates and allowances is essential for planning and staying ahead of tax obligations and investment decisions. Below are some important dates and allowances that investors and individuals should be aware of in 2025:

Tax Year & Key Deadlines

- Self-Assessment Deadline for 2023/24 Tax Year: 31st January 2025

- Filing deadline for self-assessment tax returns for the previous tax year.

- Self Assessments need to be filed for those earning above £150,000 or those who have investments/ property/ self-employed/ dividends.

- Tax Year End: 5th April 2025

Pension Contributions & Allowances for 2025

- Pension Contribution Deadline: 5th April 2025

- The last day to make contributions for the previous tax year.

- Annual Allowance: £60,000

- The maximum amount you can contribute to your pension between both yourself and your employer

- For those earning over £260,000 need to review income as may be subject to tapered pension allowance- restricting your input into pensions (lowest level is £10,000).

- Can carry back up to three years to make use of any unused allowances

Savings Allowances for 2025

- Individual Savings Account (ISA) Year-End: 5th April 2025

- The deadline to contribute your annual ISA allowance.

- ISA Annual Allowance: £20,000

- The maximum amount you can save in an ISA in a tax year.

- If you have a Lifetime ISA (LISA) then you have £4,000 allowance (this comes off of your ISA allowance).

- Personal Savings Allowance:

- Basic rate taxpayers: £1,000 tax-free on savings income.

- Higher rate taxpayers: £500 tax-free on savings income.

Don’t forget to pop these dates in your diary and for anyone who would like to have a chat about their financial planning strategy, to kick start the new year on the right foot! Please don’t hesitate to reach out!